Condensed Consolidated Income Statements For The Period Ended 30.9.2025 (unaudited)

Condensed Consolidated Statement Of Financial Position

Review of performance for the current quarter and financial period to-date

-

Despite improved fishing and aquaculture activity and stable performance of surimi-based products, MPM's current quarter sales were 11% lower than the corresponding quarter mainly due to substantially lower fishmeal sales volume affected by overall poor fish landing and depressed international fishmeal selling price.

Despite better performance of fishing, aquaculture activity and surimi based products contributed by higher volume and better margin, earnings were 19% lower than the corresponding quarter mainly due to margin erosion caused by lower fishmeal and surimi volume at depressed international fishmeal selling price.

Cumulative sales were 7% lower than the corresponding period mainly due to the same reason as the quarterly sales.

Cumulative earnings decreased by 13% mainly due to the same reasons as the quarterly earnings.

-

Despite stable sales performance of farm produce across all farming operations, ILF's current quarter sales were 10% lower than the corresponding quarter mainly due to substantially lower feed raw material trading unit price with flat volume.

Earnings were 9% higher than the corresponding quarter mainly due to stronger performance of Vietnam farming operation and stable margin of Malaysia layer operation with lower feed cost as well as improved contribution from branded egg sales which helped to cushion the impact of cost subsidy removal after the lifting of price ceiling mechanism effective 1st August 2025.

Cumulative sales were marginally lower than the corresponding period mainly due to lower feed raw material trading unit price albeit at substantially higher volume.

Cumulative earnings were marginally higher than the corresponding period mainly due to the same reasons as the quarterly earnings.

-

Despite net increase of 55 stores and 42 FM Mini, CVS's current quarter sales increased by 5% only against the corresponding quarter mainly due to lower average store sales impacted by weak consumer sentiment, exclusion of convenience store chain participation in government's Sumbangan Asas Rahmah ("SARA") program and increased competition in food and beverage market.

Earnings were 44% lower against the corresponding quarter mainly due to lower average store sales and higher operating expenses.

Cumulative sales were 6% higher than the corresponding period mainly due to the same reason as the quarterly sales.

Cumulative earnings were 24% lower than the corresponding period due to the same reason as the quarterly earnings.

-

POCE's current quarter sales were 10% lower than the corresponding quarter mainly due to extremely low CPO sales tonnage delivery caused by shipment delay under palm oil activities despite consolidation of the results of Plus Xnergy Holdings under BM Greentech.

Earnings were 48% lower than the corresponding quarter mainly due to lower solar project contribution with discontinuation of Net Energy Metering scheme ("NEM 3.0") since end June 2025 from BM Greentech as well as weaker performance of palm oil activities with lower sales.

Cumulative sales were 7% higher than the corresponding period mainly due to results consolidation of Plus Xnergy under BM Greentech.

Cumulative earnings were 20% lower than the corresponding period mainly due to the same reasons as the quarterly earnings.

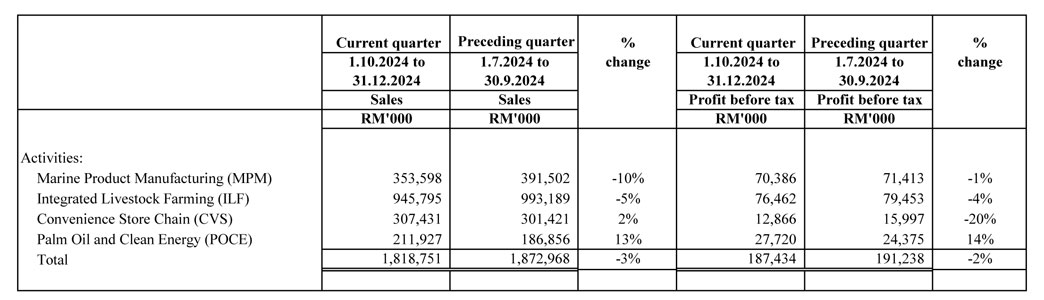

Review of current quarter performance with the preceding quarter

-

MPM's current quarter sales were 8% higher than the preceding quarter mainly due to strong performance of aquaculture activity as well as recovery in fishmeal volume and price.

Earnings were 6% higher than the preceding quarter mainly due to significant performance improvement of aquaculture activity and fishmeal while the other activities remained stable.

-

ILF's current quarter sales were marginally higher than the preceding quarter mainly due to overall higher egg selling price across all farming operations in Malaysia, Indonesia and Vietnam. In Malaysia, egg price adjusted up post lifting of the ceiling price control mechanism effective 1st August 2025.

Earnings were 57% higher against the preceding quarter mainly due to significant improvement of Vietnam farming operation as well as improved margin for other farming operations benefitting from lower feed cost and higher selling price.

-

Despite net increase of 16 stores and 7 FM Mini, CVS's current quarter sales decreased by 4% against the preceding quarter mainly due to lower average store sales after Ramadan festive peak as well as weak consumer sentiment, exclusion of convenience store chain participation in government's SARA program and increased competition in food and beverage market.

Earnings were substantially lower than the preceding quarter mainly attributed to lower average store sales and higher operating expenses.

-

POCE's current quarter sales decreased by 16% against the preceding quarter mainly due to lower solar project delivery with discontinuation of Net Energy Metering scheme ("NEM 3.0") since end June 2025 under BM Greentech and weaker performance of palm oil activities with lower CPO sales tonnage delivery caused by shipment delay.

Earnings decreased by 29% against the preceding quarter mainly due to margin compression for solar while margin normalized for bio-energy division at BM Greentech as well as lower contribution from palm oil activities with lower CPO sales tonnage delivery.

Prospects for the next quarter to 31st December 2025

Despite subdued domestic consumer sentiment caused by economic uncertainty and rising operating cost impacted by Sales and Service Tax ("SST"), the management is cautiously optimistic that the business performance will remain satisfactory in the coming quarter with its diversified and resilient nature of staple food businesses.